N

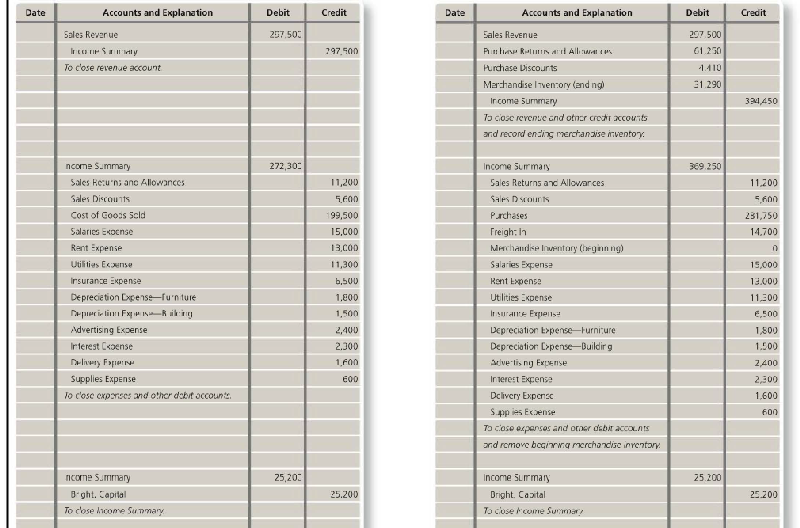

Làm ơn giải thích giùm 2 bút toán? Chênh lêch 7 500 đi vào đâu?.

Sách Applying IFRS-3e page 296-297 có đoạn như sau:

Periodic Method:

Once the count is completed, under this method the count quantities are then costed and the value of inventory brought to account. This adjustment can be done in a number of ways, but the simplest is to post the following two journal entries:

Dr Opening inventory (cost of sale) Cr Inventory 79 600

(Transfer of opening balance to expense)

Dr Inventory Cr Closing inventory (cost of sale) 87 100

(Recognition of final inventory balance)

Under the periodic method, inventory losses and fraud cannot be recorded as a separate expense. The movement in inventory balance plus the cost of purchase is presume to present the cost of sales during the reporting period.

Many thanks in advance!

Sách Applying IFRS-3e page 296-297 có đoạn như sau:

Periodic Method:

Once the count is completed, under this method the count quantities are then costed and the value of inventory brought to account. This adjustment can be done in a number of ways, but the simplest is to post the following two journal entries:

Dr Opening inventory (cost of sale) Cr Inventory 79 600

(Transfer of opening balance to expense)

Dr Inventory Cr Closing inventory (cost of sale) 87 100

(Recognition of final inventory balance)

Under the periodic method, inventory losses and fraud cannot be recorded as a separate expense. The movement in inventory balance plus the cost of purchase is presume to present the cost of sales during the reporting period.

Many thanks in advance!